|

| Inflation Protection Model Portfolio |

| Monthly Portfolio Review: March 2025Publication date: April 3, 2025 |

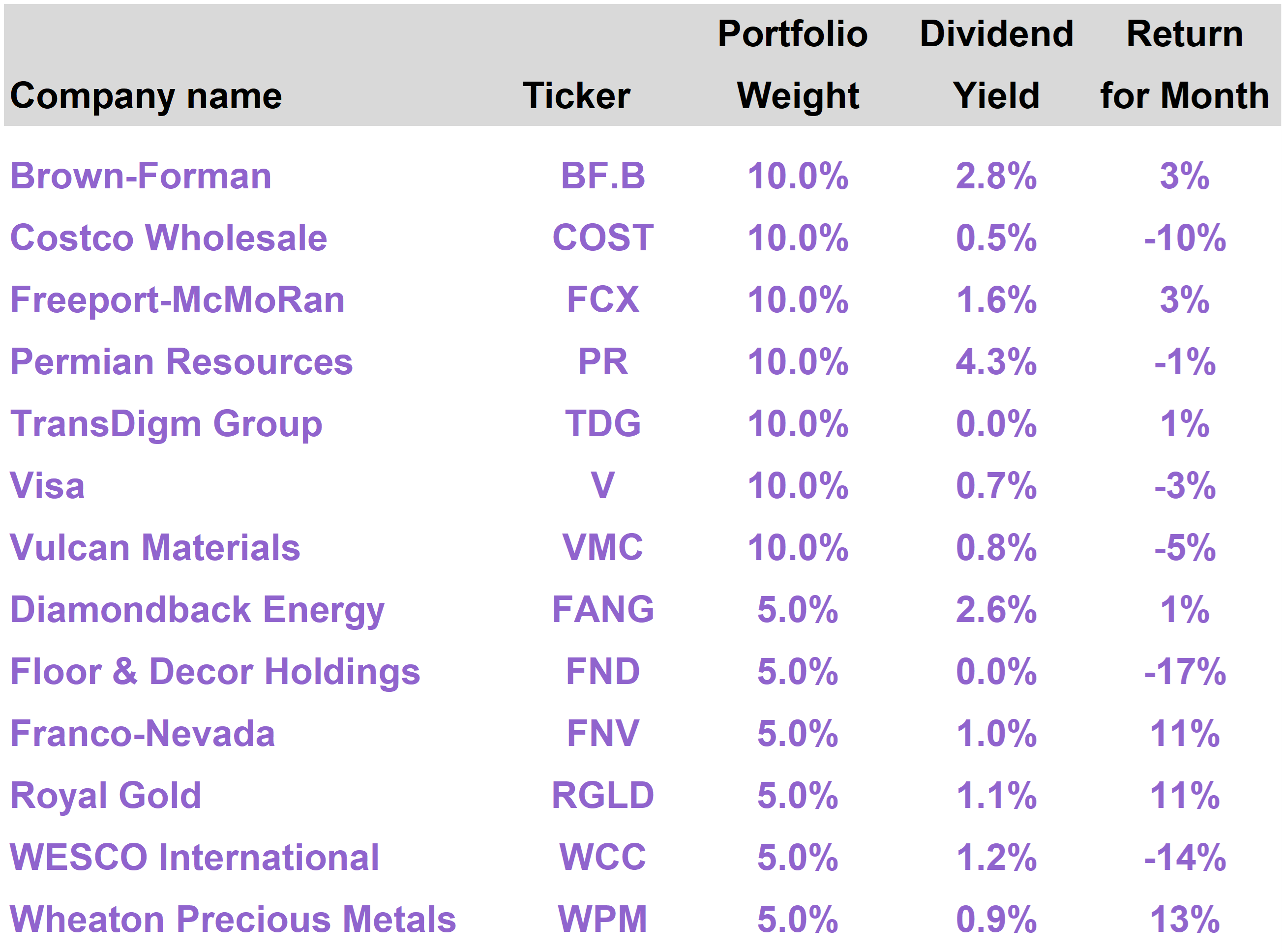

| | | Current portfolio holdings |

|  | | FOR SUBSCRIBER USE ONLY. DO NOT FORWARD OR SHARE. |

| | | The Inflation Protection portfolio generated a return of -1.0% in March, substantially better than the -5.6% total return of the S&P 500 Index. The portfolio’s gold-related investments continue to perform well and have outperformed gold, which itself has risen approximately 19% year to date through the end of March. We continue to have a positive outlook on gold as the tariff dynamic plays out, but investors may consider rebalancing into non-gold stocks now available at lower prices. More cyclically sensitive names detracted from portfolio performance during the month as risk-off sentiment prevailed. As markets react negatively to Trump’s latest tariff proposals, we encourage investors to keep a long-term focus and think opportunistically.

|

| | | The Inflation Protection portfolio returned -1.0% in March, versus a total return of -5.6% for the S&P 500 Index. On a year to date basis through the end of March, the portfolio has delivered a positive total return of 3.0%, versus -4.3% for the S&P 500.

The portfolio’s top performing stocks in March were gold-related holdings Wheaton Precious Metals (WPM), which returned 13%; Royal Gold (RGLD), which returned 11%; and Franco-Nevada (FNV), which returned 11%.

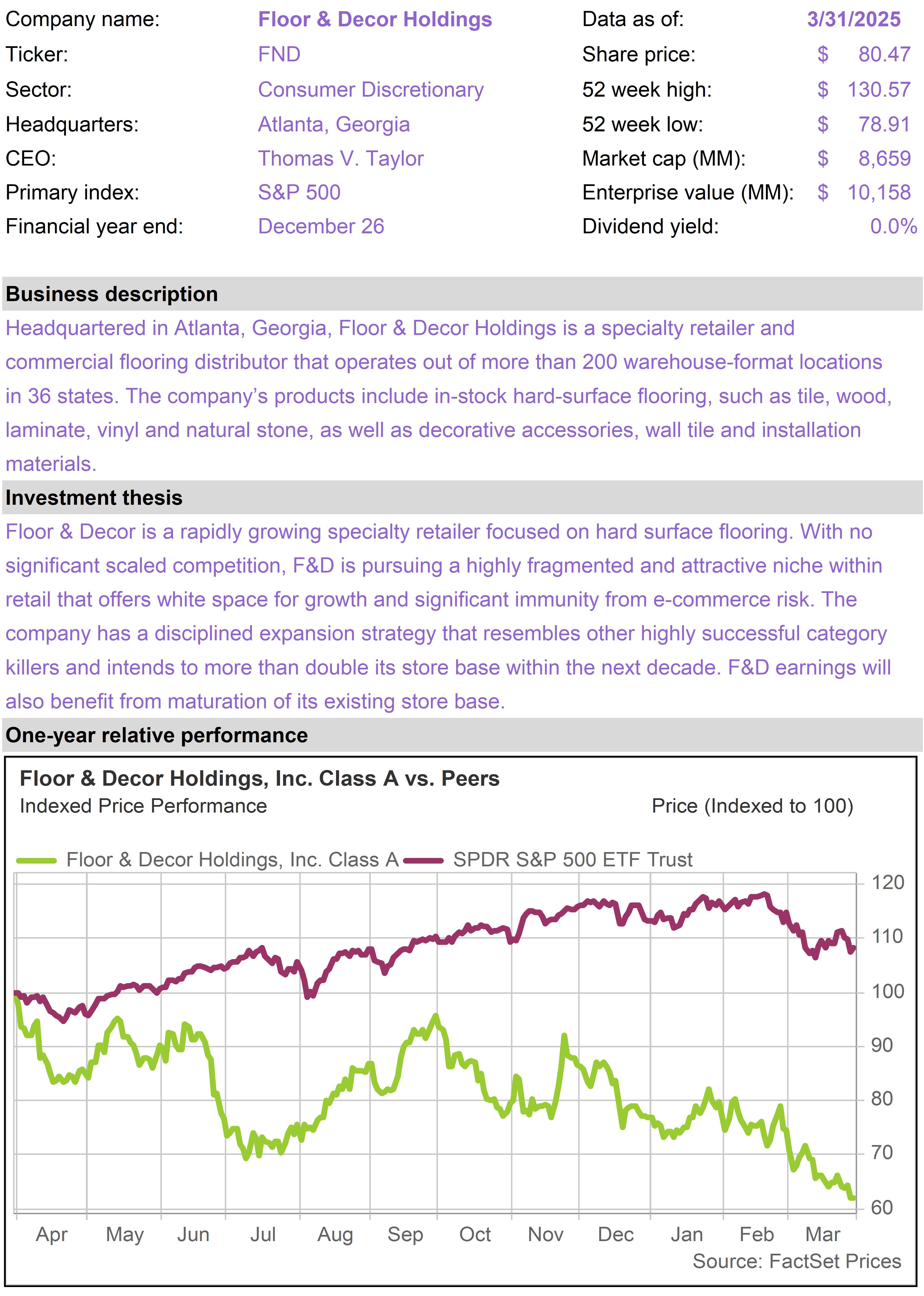

The worst performing stocks were Floor & Decor (FND), which returned -17%; WESCO International (WCC), which returned -14%; and Costco (COST), which returned -10%. |

| Tech valuations reset

After a promising start to the year, and on the heels of very strong returns in 2024 (with the S&P 500 gaining approximately 25%), March was a particularly difficult month for the stock market.

In March, we witnessed a continuation of a fairly intense sentiment shift that began towards the end of February.

As we write, this negative momentum is continuing, in the wake of yesterday afternoon’s tariff announcements. Additional commentary on these breaking developments will be provided to subscribers in the days ahead.

Optimism towards the Trump economic agenda, based on de-regulation, fiscal sanity, innovation and re-industrialization, has turned into anxiety over tariffs along with potentially disruptive federal spending cuts.

While the tech sector is not necessarily the area one would expect tariffs to impact the most, tech, especially mega-cap tech, was the part of the market that was hardest hit in March.

While the S&P 500 was down 5.6%, the tech-heavy NASDAQ Composite Index was down 8.1%. The largest tech stocks, as reflected by the Roundhill Magnificent Seven ETF (MAGS), which tracks the performance of the Mag Seven tech stocks on an equal-weighted basis, was down 10.4%. |

|  | S&P 500, NASDAQ, S&P 500 Value, Mag SevenTotal Return (March 2025) |

| It is worth noting that the S&P 500 Value Index was only down 3.0% in March. On a year to date basis through the end of March, returns on value stocks are slightly positive.

Value stocks largely consist of companies outside the tech sector that are in many cases quite sensitive to the economic growth outlook. The relative strength of value stocks suggests the volatility we saw in March was not totally driven by genuine fears of tariff-related economic collapse.

What we witnessed in March was a retrenchment of tech sector valuations, which had become quite extended and were in a vulnerable position.

Looking at the performance of the NASDAQ and Mag Seven stocks over a longer time frame puts in perspective the degree to which tech names had completely outperformed other areas of the market. |

|  | S&P 500, NASDAQ, S&P 500 Value, Mag SevenTotal Return (Last 12 Months) |

| Despite the sharp sell-off in recent weeks, Mag Seven stocks are still outperforming over the past year.

Meanwhile, the performance of NASDAQ stocks (which are a good proxy for tech and growth) is as of the end of March more or less in line with the S&P 500 (which is more balanced between growth and value) on a one-year basis.

Tariffs have been the catalyst for the negative market momentum in the tech sector, but the stage was set by dramatic tech outperformance that began in earnest in September 2024 and extended all the way to mid-February 2025.

Rotation to international

Just as investors in recent weeks have moved money out of highly valued tech shares into other industries, we also saw strong performance in international stocks.

While the S&P 500 was down 4.3% in the first quarter of 2025, developed market international stocks (as measured by the MSCI EAFE Index) were up 7.0%. |

|  | S&P 500, NASDAQ, International StocksTotal Return (Last 3 Years) |

| International stocks had badly lagged U.S. stocks for most of the past year, until mid-February, thanks in no small part to the sharp rally in tech shares.

But if we look at relative performance on a three-year basis, the performance gap between the U.S. and international stocks has now largely disappeared.

Put differently, as a result of this recent tech-led sell-off, U.S. stocks have “caught down” to international stocks—at least on a three-year basis.

Inflation concerns

In addition to tariffs, concerns about persistent inflation have also hurt investor sentiment. Last week’s Personal Consumption Expenditures Price Index (PCE) reading, which came in slightly above expectations, contributed to selling pressure.

As we discussed over the weekend on our livestream, while sticky inflation is a strong media narrative, especially as it relates to tariffs, actual bond market inflation expectations tell a different story. |

|  | Despite a lot of speculation about tariffs being highly inflationary, market-based inflation expectations, as inferred from Treasury Inflation-Protected Securities, remain low. |

|  | Long-term Inflation Expectations(Last 12 Months) |

| The 5-Year, 5-Year Forward Inflation Expectation Rate represents the average inflation rate (over the five year period beginning in five years) that is being priced in by investors in U.S. Treasuries.

This forward inflation rate is now approximately 2.1%, quite close to the Federal Reserve’s target level of 2%.

The key takeaway is that the bond market is not signaling any reason to panic on the inflation front.

Mag Seven drove sector performance

Similar to February, the Technology sector led the way down in March, while other industry sectors that have large exposure to technology-related companies also fared poorly.

Consumer Discretionary stocks, for example, suffered because Tesla (TSLA) and Amazon (AMZN) are the two largest names in that sector. TSLA and AMZN shares declined 12% and 10% respectively in March. |

|  | | Similarly, the Communications Services sector has Magnificent Seven constituents Meta (META) and Alphabet (GOOGL) as its two largest holdings. These stocks represent close to 40% of the total market capitalization of the sector.

META and GOOGL shares declined 14% and 9% in March.

More defensive sectors, such as Utilities, Consumer Staples and Health Care, performed relatively well. Their earnings are perceived as less vulnerable to an economic slowdown, while their valuations benefit from declining long-term interest rates.

Liberation Day fall-out

Yesterday evening, President Trump rolled out his reciprocal tariff plans.

There had been some optimism in the market this week that the tariff policy would be gentler than previously feared. However, the proposed levels are generally seen as higher than expected.

As markets come under pressure, we will keep subscribers up to speed on our latest thinking through the usual channels. |

| | | In March, the top performing stocks in the Inflation Protection portfolio were Wheaton Precious Metals (WPM), which returned 13%; Royal Gold (RGLD), which returned 11%; and Franco-Nevada (FNV), which returned 11%.

The most significant portfolio detractors this month were Floor & Decor Holdings (FND), which declined 17%; WESCO International (WCC), which declined 14%; and Costco (COST), which declined 10%. |

| The portfolio’s gold-streaming plays performed quite well and functioned as an excellent portfolio hedge. Gold itself increased approximately 9% in March.

On a year to date basis, gold is up approximately 19% through the end of March, while the portfolio’s gold-streaming stocks (WPM, RGLD and FNV) are all substantially outpacing the strong performance in gold. |

|  | We revisited the case for gold, especially as a diversifier within stock portfolios, on our recent livestream, which can be accessed here.

Gold is benefiting from an enduring trend among central bankers, especially in emerging markets, to build up their gold reserves and reduce their exposure to the U.S. dollar and U.S. Treasuries.

Gold is also benefiting from the ongoing tariff dynamic in multiple ways.

The Trump administration is focused on reducing its trade deficits with the rest of the world and is biased toward policies that tend to reduce the value of the U.S. dollar relative to other world currencies.

Foreign central banks are keen to continue to amass gold as uncertainty grows with respect to their holdings of dollar-denominated assets.

Gold is also benefiting from the general climate of uncertainty created by the tariff situation, which is taking the global economy into largely uncharted waters.

Tariffs also create incentives for countries to embrace easier monetary policies (i.e., money printing) as they seek to overcome the negative impact of tariffs with lower exchange rates.

Interest rates have also been coming down as the tariff dynamic has played out on concerns of slower growth. This has added another layer of support to the gold price as it reduces the opportunity cost of owning gold relative to fixed income investments.

We continue to favor an allocation to gold as reflected in the portfolio’s current 15% allocation to gold-related investments. However, investors who have benefited from upside in these gold names (pushing their gold allocation beyond the 15% threshold) may consider rebalancing.

The beauty of gold in a portfolio context is that it often holds its value or rises in periods of stock market volatility. This creates the opportunity to recycle gold upside into non-gold stocks which are available at lower prices.

As smaller companies with cyclical exposure, FND and WCC fared poorly in the March sell-off. Despite the volatility, we continue to believe in the long-term prospects of these businesses.

Having substantially outperformed the overall stock market over the past two years, COST shares underperformed in March following its second quarter earnings report.

Top line revenue results were well received, but earnings slightly missed, partly as a result of foreign exchange rates (which should become less of an issue with recent dollar weakness).

As we are potentially entering a period of heightened volatility, we encourage subscribers to stay focused on the long-term fundamentals of strong businesses rather than market headlines.

Periods of risk aversion, like the current one, often produce excellent entry points for long-term investors in high quality stocks. |

| | |  | | |  | | |  | | | |  |  | | |  |  | | |  |  | | |  |  | | |  |  | | |  |  | | |  |  | | Diamondback Energy (FANG) |

|  |  | | Floor & Decor Holdings (FND) |

|  |  | | |  |  | | |  |  | | WESCO International (WCC) |

|  |  | | Wheaton Precious Metals (WPM) |

|  |  | | The 76research Inflation Protection Model Portfolio emphasizes business models that are expected to perform well on a relative basis in periods of elevated inflation. Holdings are typically selected from industries based on supply constrained real assets, including commodity and energy businesses, or companies that otherwise demonstrate superior pricing power. Drawing from an investable universe of expected inflation beneficiaries, specific holdings are chosen based on valuation and general business quality, growth and risk considerations. |

| | FOR SUBSCRIBER USE ONLY. DO NOT FORWARD OR SHARE. |

| | | |  |

|

|

|

| |

|