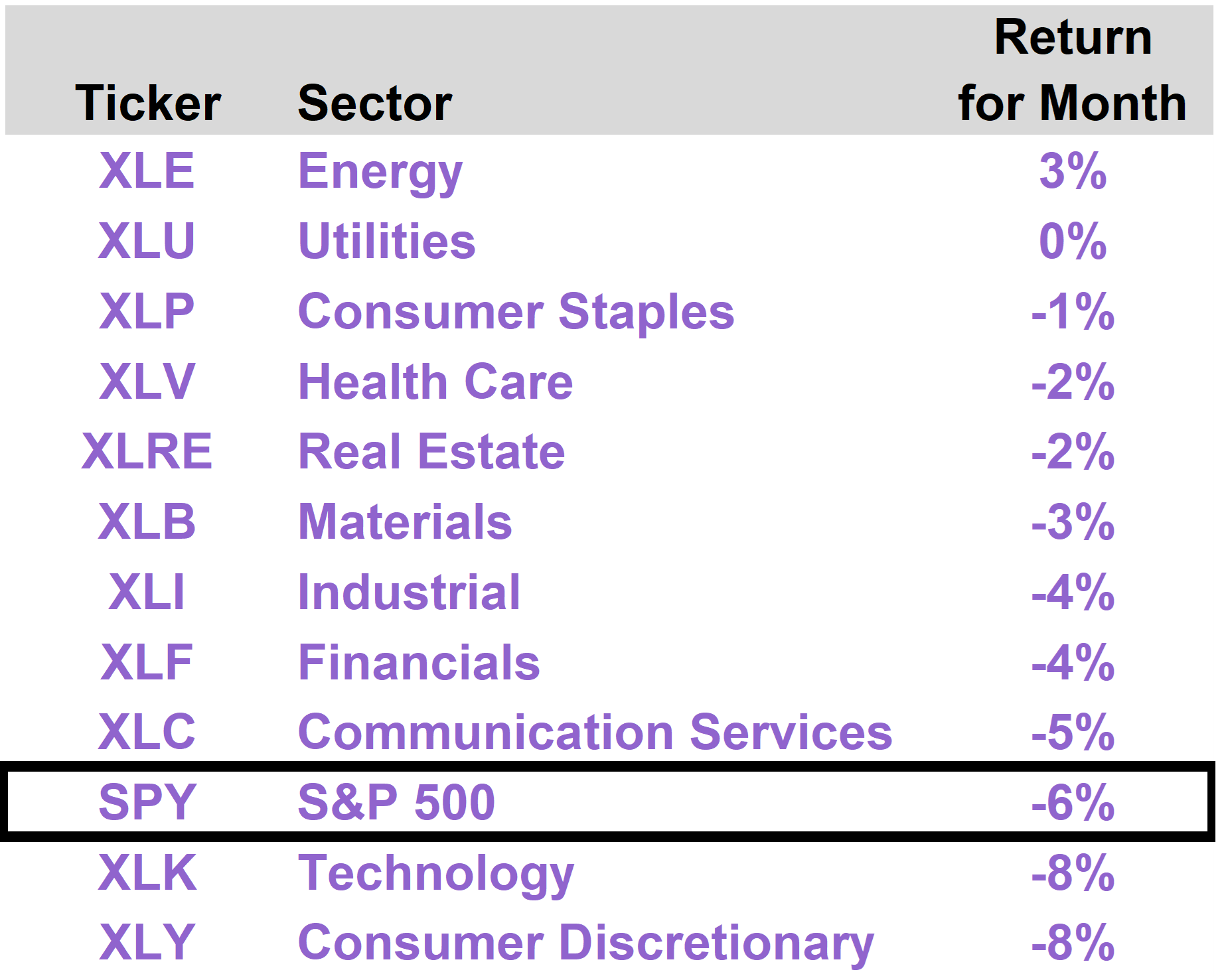

Shares of communications tower operator CCI outperformed in March for two main reasons.

First, the company announced in the middle of the month that it has entered into an agreement to divest its “small cell” fiber business on attractive terms.

Many investors, including some activists, were pushing for the sale of this business, which was viewed as a distraction from the company’s core business of providing communication tower access to the mobile phone industry.

Proceeds of the sale will be used to buy back shares and reduce debt. In connection with the transaction, the dividend was trimmed, but CCI shares still offer a close to 5% dividend yield.

Second, with a business model based on long-term contracts with high quality tenants (the largest telecommunications providers in the U.S.), CCI stands out as a defensive stock with bond-like characteristics. CCI shares perform well in risk-off environments and periods of declining long-term interest rates.

KMI and WMB shares performed relatively well in recent weeks with some assistance from firmer energy prices, which benefited the Energy sector generally.

As the two leading natural gas infrastructure players in the U.S., KMI and WMB continue to be viewed as significant beneficiaries of the Trump policy agenda. They benefit from not only a solid demand outlook for their existing networks of natural gas pipelines but expansion opportunities as well.

The almost insatiable electrical power requirements of the many large-scale AI data centers under construction throughout the U.S. represent a key demand driver for natural gas.

To the extent tariffs stimulate an expansion of energy-intensive domestic industrial activity, this should only bolster demand for natural gas that is already supported by the AI buildout.

Whereas a stock like CCI will tend to perform well in risk-off scenarios, alternative asset managers BX and CG tend to underperform as somewhat leveraged plays on the broader market.

We continue to view both BX and CG as excellent long-term compounders. We would expect both names to outperform in the context of a general market recovery.

We published a note in the 76report earlier this month (High Yield with Bitcoin Upside) on Strategy Convertible Preferred Stock (STRK). Offering an approximately 9% dividend yield, we believe this security may be particularly interesting to Income Builder subscribers.

As the first and by far largest Bitcoin Treasury Company, Strategy is a unique company, and STRK is a unique security.

For investors who are deeply skeptical of Bitcoin’s long-term viability, STRK is likely to be of little interest.

However, for investors who have confidence in Bitcoin as an asset, STRK is intriguing in our view because of how immensely overcollateralized Strategy is in terms of its Bitcoin holdings relative to its dividend and interest obligations.

We also find it interesting and comforting that STRK trades with surprisingly low correlation to MSTR common stock and the price of Bitcoin.

Investors seem to understand that even material fluctuations in MSTR and Bitcoin do not really impact the company’s ability to live up to its dividend commitments to STRK holders.

As we now find ourselves in a period of heightened volatility, we encourage subscribers to stay focused on the long-term fundamentals of strong businesses rather than market headlines.

Periods of risk aversion, like the current one, often produce excellent entry points for long-term investors in high quality stocks.