The top performing stocks in the portfolio in March were Williams (WMB) and Arch Capital Group (ACGL), which each returned 4%.

The worst performing stocks in the portfolio were Oracle (ORCL), which returned -16%, and Costco (COST), which returned -10%.

Shares of NVIDIA (NVDA) performed poorly over the course of March, down 13%, but were basically flat since we added NVDA to the portfolio in the middle of the month. (The March 12 portfolio update report on NVDA can be accessed here.)

As emphasized above, the last six weeks or so have been an extremely difficult stretch for Mag Seven stocks, including NVDA.

While the Mag Seven are in many ways exceptional companies, we have previously been reluctant to include them in the portfolios because of valuation concerns. In the case of NVDA, the steep decline in recent weeks has led us to revisit that position.

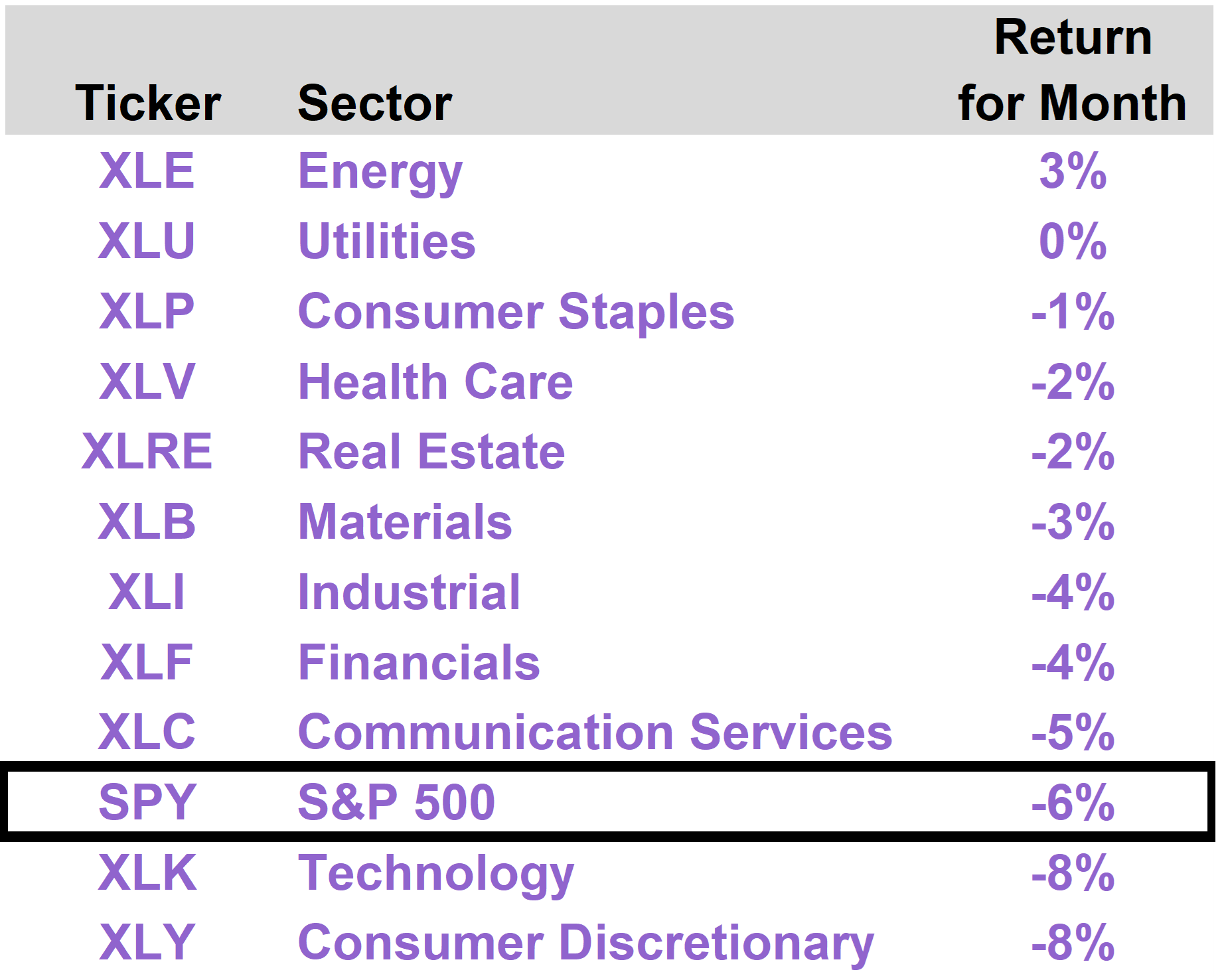

WMB shares performed relatively well in recent weeks with some assistance from firmer energy prices, which benefited the Energy sector generally.

As the leading natural gas infrastructure player in the U.S., WMB continues to be viewed as a significant beneficiary of the Trump policy agenda. WMB benefits from not only a solid demand outlook for its existing network of natural gas pipelines but expansion opportunities as well.

The almost insatiable electrical power requirements of the many large-scale AI data centers under construction throughout the U.S. represent a key demand driver for natural gas.

To the extent tariffs stimulate an expansion of energy-intensive domestic industrial activity, this should only bolster demand for natural gas that is already supported by the AI buildout.

ACGL is a well-managed and highly profitable property and casualty insurer and reinsurer. The share price has been supported by robust cash flow generation and disciplined share repurchases.

Shares of ORCL were down in March, consistent with the performance of other large-cap tech names.

ORCL shares started to gain momentum following a strong outlook provided in the mid-March third quarter earnings report, but they were ultimately brought down with the broader market weakness by the end of the month.

Notably, ORCL reported 60+% growth in its order book. This does not include any contribution from Trump’s Stargate initiative.

Similar to NVDA, ORCL is likely to see robust earnings growth over the next several years (and beyond) on the strength of AI-related spending. With the recent reversal of market sentiment, ORCL now trades with a very attractive valuation (approximately 18x FY 2026 consensus earnings).

Having substantially outperformed the overall stock market over the past two years, COST shares underperformed in March following its second quarter earnings report.

Top line revenue results were well received, but earnings slightly missed, partly as a result of foreign exchange rates (which should become less of an issue with recent dollar weakness).

As we are potentially entering a period of heightened volatility, we encourage subscribers to stay focused on the long-term fundamentals of strong businesses rather than market headlines.

Periods of risk aversion, like the current one, often produce excellent entry points for long-term investors in high quality stocks.