Stocks suffered another big setback yesterday as Donald Trump escalated his feud against Fed Chair Jerome Powell. This new threat to central bank independence has only exacerbated already rattled investor confidence in the U.S.

The S&P 500 declined 2.4%, with the tech-heavy NASDAQ performing slightly worse, down 2.6%.

Through yesterday, the S&P 500 has given up most of its gains since Trump announced his 90 day tariff pause. The S&P 500 is now less than 4% above its lowest levels of the year just prior to the pause.

As frustrating as this year has been, investors with adequate liquidity and a long time horizon have the opportunity to buy high quality U.S. stocks at prices that may seem quite attractive in the future.

Meanwhile, we continue to favor gold and Bitcoin exposure as portfolio hedges. Both assets should benefit from dollar weakness and what will likely become a global shift towards easier monetary policy if the growth outlook continues to deteriorate.

First tariffs, now this

Coming on the heels of a tariff debacle that remains unresolved, the battle over control of the Fed opens a fresh wound.

The issue is not so much who is right or wrong about whether or not interest rates should be cut at the moment.

Trump may have some valid points. “Too Late” Powell may indeed be under-reacting with his “wait and see” approach.

The issue is the institutional independence of the Fed and Trump’s willingness to respect the letter and the spirit of the law. In theory, Powell can be fired by the President as Chair “for cause,” but not for mere policy disagreements.

An independent central bank is widely viewed as the cornerstone of an investable market. It is a key area of focus for investors in emerging markets. Investors in a major developed markets usually just take it for granted.

When politicians can direct central bankers to do their bidding, the economic environment becomes unpredictable. Trust is lost.

The U.S. has historically been seen by investors as providing the legal and political foundation of the entire global financial system.

Investors expect stability and predictability from the U.S. They do not like to see a President even contemplate legally murky maneuvers to eject a Fed Chair just because he wants easier monetary policy.

While the Fed and the Executive Branch are separate entities, and the Supreme Court would likely rule that should push come to shove, Trump is not wrong to want lower rates.

Inflation is low, and new data suggests economic trouble on the horizon. Nonetheless, Powell will likely be reluctant to move until he sees multiple data points pointing to rising unemployment.

Capital flight

What we have witnessed over the past several weeks is a wholesale exodus from U.S. capital markets.

We see this in stocks, which have declined sharply.

We see this in government bonds, where long-term yields in the U.S. have risen, even though they typically fall when recession risk rises.

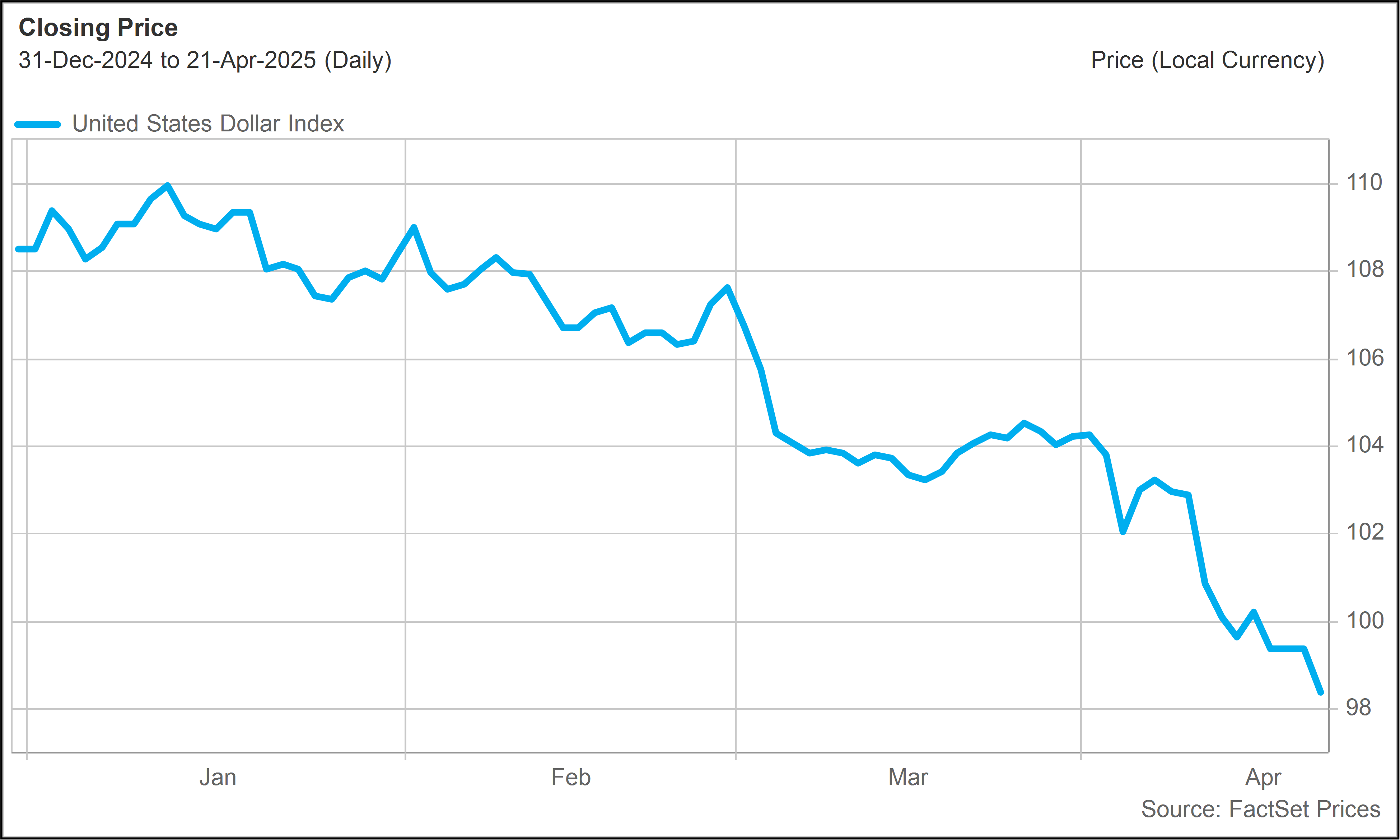

We see this in the U.S. dollar. The Dollar Index (DXY), which measures the U.S. dollar versus a basket of major foreign currencies, is now down more than 9% on a year to date basis.

We also see it in the price of gold and more recently in Bitcoin.

Gold has advanced some 25% year to date.

Bitcoin, which had been declining with stocks, has reversed course and has significantly outperformed U.S. stocks since the beginning of April.

From hero to zero

It was less than ten weeks ago (February 19, 2025 to be exact) that the S&P 500 (and by extension, U.S. economic exceptionalism) reached an all-time high.

Investors were heavily focused on the AI opportunity and its potential to drive growth and productivity across the entire economy.

Now, instead of conversations about the U.S. dominating the technologies of the future, we are talking about reshoring textile mills from Vietnam.

What the heck has happened?

Because the market narrative has shifted so abruptly, we are currently witnessing a severe reallocation of capital in a very rapid time frame.

In the months that followed the election, global investors were pouring money into the U.S. stock market.

Just four weeks before the market peaked, legendary investor Stan Druckenmiller told CNBC: “I’ve been doing this for 49 years, and we’re probably going from the most anti-business administration to the opposite. So we do a lot of talking to CEOs and companies on the ground, and I’d say CEOs are somewhere between relieved and giddy.”

Druckenmiller went on to comment that business confidence was at record levels and that the economy looks “very, very strong at least for the next six months.”

Investors for the most part were also giddy. Now they are dismayed.

Whiplash

The rapid decline in the Dollar Index tells the story. The downward pressure seen in the dollar this year began as markets responded to Trump’s tariff initiatives.

Speculation over tariffs picked up steam in March. The dollar then saw another leg down after Liberation Day on April 2.